Changes in Definitions of Israeli Resident and Foreign Resident – The End (?)

Since 2003, Israeli law has defined the tax residency of individuals determined based on a facts and circumstances “center of life” test which supersedes the physical presence presumptions included in the Income Tax Ordinance.

In recent days, a new proposal was published that simplifies the definitions of “Israeli Resident” and “Foreign Resident” for individuals. The proposal aims to reduce the scope of disputes regarding the residency of individuals, by establishing absolute quantitative presumptions which are likely to provide a clear answer in many cases of disputed residency.

Note, that this is not the first time that a similar proposal was advanced by the ITA. In August 2023, a legislative proposal was published aiming to reform the criteria which also included a strong emphasis on quantitative presumptions. However, this proposal was never legislated into law.

Proposed Amendment:

The proposed amendment establishes absolute presumptions that cannot be refuted. If these tests are met, the individual will be considered an Israeli resident or a foreign resident and will not be able to argue that his “center of life” leads to a different conclusion. However, it should be noted that even if the amendment is legislated, there will be cases where none of the absolute presumptions apply. In such cases, the residency of the taxpayer will be examined according to the current “center of life” test as developed by Israeli case law.

The examination of the quantitative presumptions will be both for the tax year in question and for a “Three-Year Period” which will be defined as one of the following:

For the purposes of determining the number of days spent in Israel in a “Three-Year Period”, the proposal uses a “weighted average”.

The amendment does not change the rule established in case law that a part of a day spent in Israel is considered a full day.

Absolute Presumptions of Israeli Residency:

The amendment proposes that an individual will be irrefutably determined to be an Israeli resident in one of the two following situations:

Proposed Amendment Absolute Presumptions – Foreign Resident:

The amendment proposes that an individual will be irrefutably determined to be a Foreign Resident in one of the two following situations:

Example:

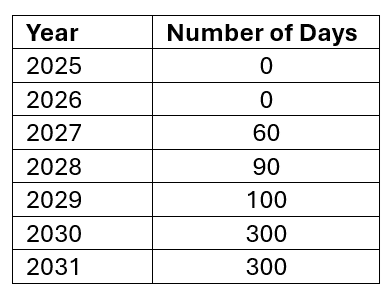

Oliver (who is single) stayed in Israel the following number of days:

We will examine whether Oliver is an Israeli resident or a foreign resident in each of the years 2027 – 2029.

Year 2027:

In tax year 2027 Oliver spent 60 days in Israel. Therefore, there will not be an absolute presumption that he is a resident of Israel. However, Oliver might be considered a foreign resident under the absolute presumption if the Three-Year Period day count is 110 days or less.

For tax year 2027 there are three possible Three Year Period, 2025 – 2027, 2026 – 2028, 2027 – 2029:

For the first Three Year Period (2025 – 2027) the calculation will be 0 + 0 + 60 or 60 days.

For the second Three Year Period (2026 – 2028) the calculation will be 0 + 60 + 1/3 * 90 or 90 days.

For the third Three Year Period (2027 – 2029) the calculation will be 60 + 1/3 * 90 + 1/6 * 100 or 106.6 days.

In 2027, Oliver will be considered a foreign resident according to the absolute presumption as he has spent less than 75 days in Israel and his Three Year Period calculation is 110 days or less in every alternative.

Year 2028:

In 2028 Oliver has spent 90 days in Israel so that he cannot be determined to be a foreign resident under the absolute presumption. However, he could be viewed as an Israeli Resident if his day count any of the possible Three-Year Periods amounts to 183 days or more.

Alternative 1 of the definition of the Three-Year Period = 1/6*0 (2026) + 1/3*60 (2027) + 90 (2028) = 110.

Alternative 2 of the definition of the Three-Year Period = 1/3*60 (2027) + 90 (2028) + 1/3*100 (2029) = 143.3.

Alternative 3 of the definition of the Three-Year Period = 90 (2028) + 1/3*100 (2029) + 1/6*300 (2030) = 173.3.

In 2028, Oliver does not meet the absolute presumptions of an Israeli resident and does not meet the absolute presumptions of a foreign resident. In this case, Oliver’s residency in 2028 will be examined according to the “center of life” test.

Year 2029:

In 2028 Oliver has spent 90 days in Israel so he cannot be determined to be a foreign resident under the absolute presumption. However, he could be viewed as an Israeli Resident if his day count any of the possible Three-Year Periods amounts to 183 days or more.

Alternative 1 of the definition of the Three-Year Period = 1/6*60 (2027) + 1/3*90 (2028) + 100 (2029) = 140.

Alternative 2 of the definition of the Three-Year Period = 1/3*90 (2028) + 100 (2029) + 1/3*300 (2030) = 230.

Alternative 3 of the definition of the Three Year Period = 100 (2029) + 1/3*300 (2030) + 1/6*300 (2031) = 250.

In 2029, Oliver will be considered an Israeli resident according to the absolute presumption.

Additional Issues

For more details, you can contact Adv (CPA) Doron Elmekiesse from our office.

Join Newsletter

Join Newsletter