Congratulations (or maybe not)!!! You are an Israel Resident: A Bill Proposing New Definitions and Presumptions for Establishing Israeli Residency for Taxpayers

The draft bill[1] to reform determining tax residency in Israel is expected to lead to nothing short of a revolution regarding how an individual can be considered an Israel Resident, or alternately a Foreign Resident, for income tax purposes.

The Amendment’s objective is to minimize the scope of existing disputes regarding an individual’s residency, and to set forth irrefutable presumptions based on the number of days an individual spent inside and outside of Israel, in order to decide the resulting tax liability in Israel.

The current status:

Today, the legal status prescribes that residency is decided based on the “center of life” test, a qualitative individual test that examines the taxpayer’s center of life. Thus, the totality of the taxpayer’s personal, familial, and economic ties are examined. For example, the location of their permanent home, where their family members study, whether and where they are active in various organizations or unions, and what and where their financial interests are, are all examined.

In order to simplify the “center of life” test, rebuttable presumptions have been set forth, under which an individual is presumed to be an “Israel Resident”. Thus, these presumptions place the burden of proof upon whoever seeks to refute them, the taxpayer/Tax Authority (as relevant). However, in any event, these presumptions are refutable.

Rebuttable presumptions – Present law

The proposed amendment:

The proposed Amendment introduces extreme cases in which irrefutable presumptions, can be implemented. Where these are met, the individual will be viewed as an Israel Resident or a Foreign Resident. It is important to note that the Amendment adds these presumptions to the existing law. Thus, following the Amendment, there will be extreme cases that cannot be appealed, and it will no longer be possible to argue that the “center of life” test leads to a different conclusion. And in contrast to these, in cases where there are no irrefutable presumptions, the taxpayer’s residency would still be examined according to the center of life test, using the rebuttable presumptions (where relevant), with respect to which the burden of proof would be upon the entity arguing against the presumption.

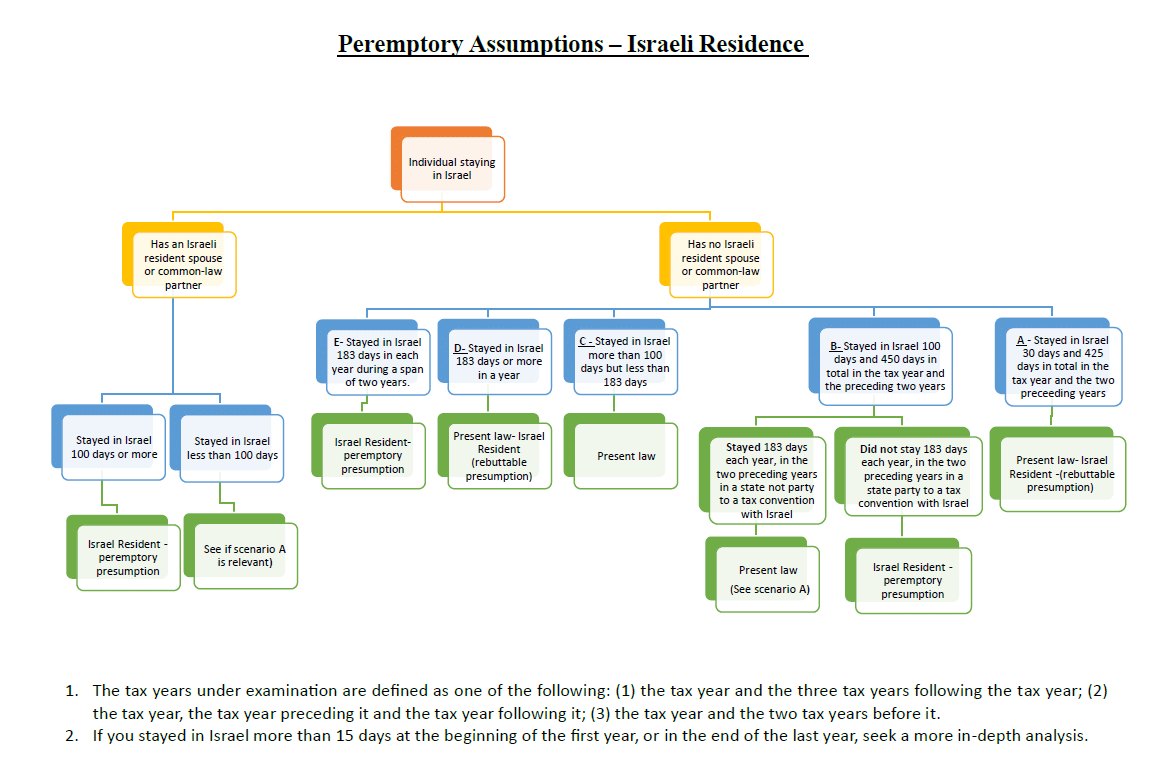

Proposed amendment – irrefutable presumptions – Israel Resident

Example of an irrefutable presumption – Israel Resident – A significant change is the requirement for confirmation of residence from a reciprocating state (a state that has an international tax convention with Israel). Thus, for example, in a case where a person stayed in Cyprus for 183 days every year during three years, and stayed in Israel 450 days during these three years (presumption no. 2 above), they would be considered an Israel Resident according to an irrebuttable irrefutable presumption, since Cyprus is not a reciprocating state. Even in a parallel case where this person did stay in a reciprocating state (such as the United States), yet for some reason or another, they are not considered a resident there; the Israel Tax Authority would consider them an Israel Resident.

Additional example – We would like to mention another example of a significant change in the bill, and that is the emphasis placed upon the spouse or common law partner’s place of residence. The Amendment proposes to stipulate an irrefutable presumption with respect to a person who stayed in Israel for 100 or more days, and their spouse including a common-law partner, was an Israel Resident (according to the peremptory/rebuttable presumptions or the center of life test).

In other words, even a person who stayed in Israel less than 183 days, and according to the present law would not be an Israel Resident (according to the center of life test/rebuttable presumptions) would now be considered an Israel Resident according to an irrefutable presumption because they have marital ties with an Israeli partner, including where these taxpayers are not officially married but rather are common-law partners.

Conclusion – In conclusion, the draft bill is intended to minimize uncertainty regarding residency in ostensibly clear cases, where it appears the taxpayer is clearly an Israel Resident or, alternately a Foreign Resident. However, these changes create new exposure even for taxpayers the Tax Authority did not view as Israel Residents thus far.

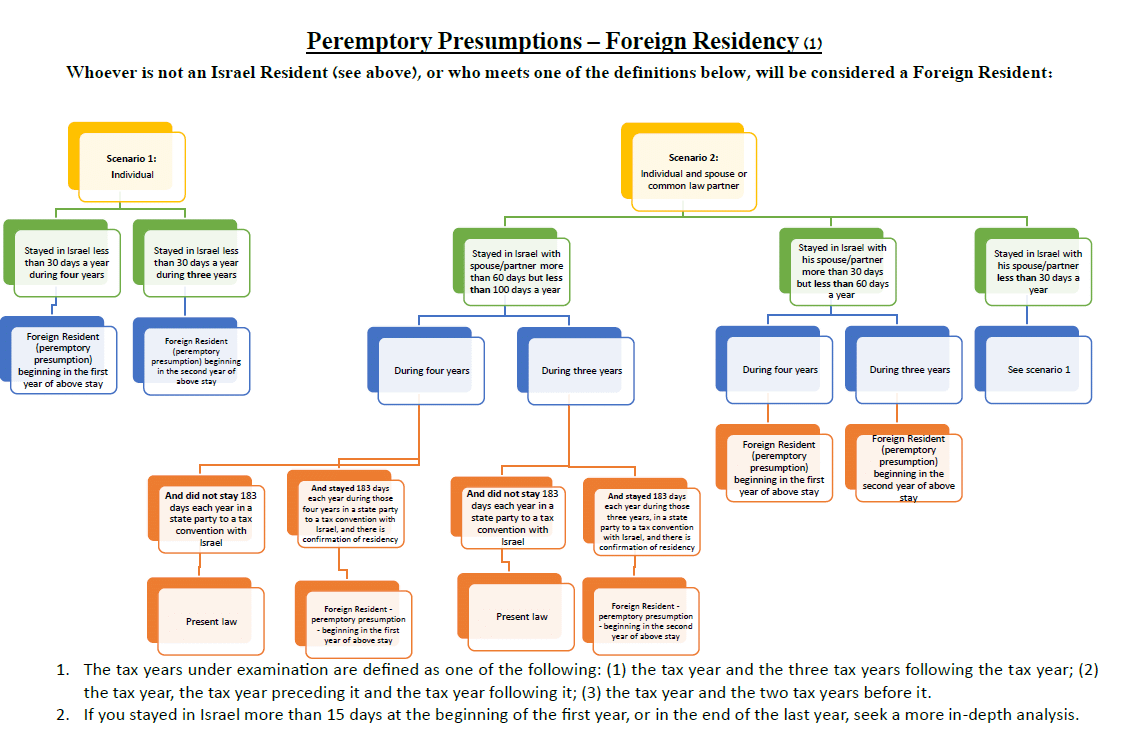

In order to minimize the uncertainty, two flowcharts are enclosed in this circular – one for examining whether a person is an Israel Resident, and the other for examining if the person is a Foreign Resident, all according to the above draft bill.

For additional information, contact Adv. (CPA) Doron Elmekiesse from our firm.

[1] Draft Bill to Amend the Income Tax Ordinance (Amendment No….) (Individual’s Place of Residence), 5783-2023 (hereinafter: the “Amendment”).

Join Newsletter

Join Newsletter